The Business Council of British Columbia (BCBC) says it is “deeply concerned about the expected economic slowdown and rapid deterioration in the province's fiscal position” as outlined in the B.C. government's First Quarterly report released September 27.

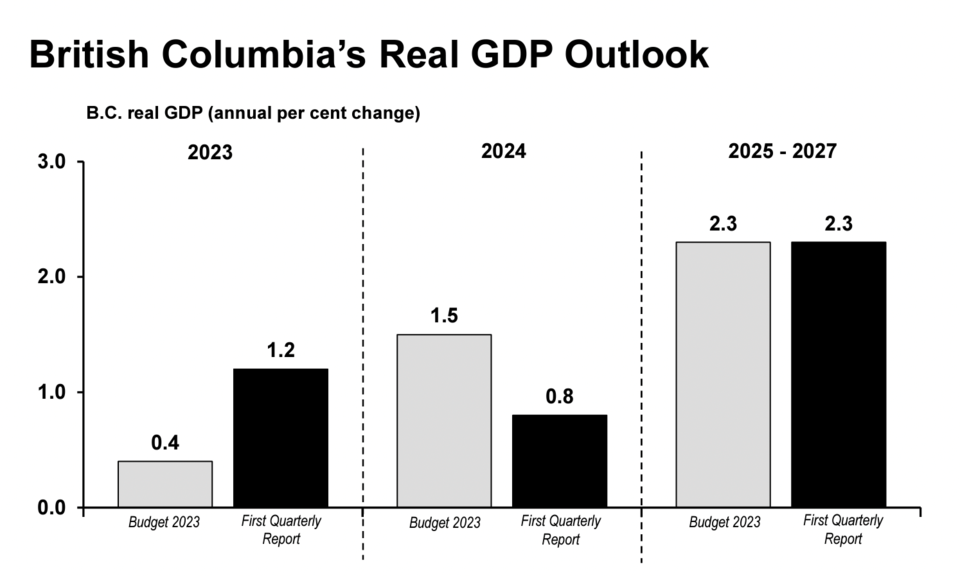

The fiscal update predicts B.C. is headed for a period of weak economic growth as the export sector slows and the massive lift flowing from the construction of large capital projects fades. The economic growth outlook for this year was revised upwards, but the outlook for 2024 was significantly downgraded. Instead of growing by 1.5 per cent, the government now expects B.C.’s economy to grow by a mere 0.8 per cent next year. This moves British Columbia from being one of Canada’s growth leaders to close to the bottom of provincial growth rankings.

Real per capita income is forecast to decline 2 per cent this year and another 2 per cent in 2024/25.

“Income declines of this magnitude only occur during recessions in B.C.; two large consecutive declines are particularly unusual,” the BCBC noted in a release.

“The amount of income per person generated in the B.C. economy is on track to fall back to where it was five years ago in 2017-2018.” said Ken Peacock the Business Council’s chief economist. “This is moving us in the wrong direction and making many people at the grocery store and gas pumps feel they are falling behind, because the unfortunate reality is they are,” he continued.

The Business Council believes the economy must become the government’s top priority. Without additional investment and stronger economic growth, many B.C. households will continue to confront falling living standards in the next few years.

“The current path looks bleak but there is an alternative, we can get serious about fast-tracking projects in all sectors from LNG and mining to AI and biotechnology that create and sustain high-paying jobs,” said Laura Jones, President and CEO. “The importance of growing the economy can’t be overstated. Growth gives us hope and means more resources for everything from hiring more teachers to developing more social housing. Shrinking economies force tough trade-offs that no one wants to face like which programs get less,” she continued.

The quarterly update also shows revenue shortfalls and higher than planned spending have pushed the projected deficit up significantly from $4.2 billion to $6.7 billion in fiscal 2023/24. The deficit is now forecast to be more than $1 billion larger than the deficit incurred during the 2020/21 pandemic year.